After the clock struck midnight last Thursday the last lion of the Senate Republican John McCain, drove a stake through the heart of the Senate Republican repeal Obamacare bill. This leaves repeal efforts deader than the “death spiral” Republicans claim Obamacare is in. Does this mean American healthcare is in chaos? Will insurance companies pull out of more states? Will premiums and deductibles grow through the roof? Yes, yes and yes unless Democrats are willing to make healthcare compromises to repair Obamacare.

Take a look as Senator John McCain deals the death blow to Republican repeal of Obamacare

He, Senator Susan Collins and Senator Lisa Murkowski took the heroic vote opposing their fellow Republicans to block the sham reform bill meant to deny millions healthcare.

Democrats must now vindicate the 3 heroes by coming forth with healthcare proposals to repair Obamacare. Minority Leader Chuck Schumer’s spoken words after the death dealing vote to repeal struck the right tone, check it out

In keeping with Senator Schumer’s words there are 3 healthcare compromises Democrats can make to repair Obamacare.

1) Repeal the business mandate on companies with 50 or more employees

Companies with 50 or more employees should no longer be required to offer health insurance, however those that voluntarily offer it should still be required to offer plans that offer the 10 essential benefits. According to a study done by the Urban Institute “Why Not Just Eliminate the Employer Mandate?” The benefits to employees from the employer mandate are negligible. The Urban Institute found that close to two-thirds of America’s workers already had coverage through their employers, regardless of the mandate.

Employers have an incentive to offer coverage because of tax benefits, and because these benefits attract high-quality workers that might otherwise choose to work elsewhere. Through most employer-provided health plans, workers receive nontaxable compensation in the form of health plans. If employers did not offer health insurance, employees would likely receive a higher, taxable salary and could purchase coverage through the Obamacare exchanges.

The Urban Institute found that the number of employers offering coverage, and the number of workers receiving coverage through their employers under Obamacare would not change much if the employer mandate were to be eliminated. If the mandate were removed, the number of workers receiving employer-based health coverage would fall by just 0.3 percent. This would be one of the least painful healthcare compromises Democrats could make.

2) Allow flexible essential benefits for millennial insurance policies only

The Affordable Care Act established a set of 10 categories of services health insurance plans must cover, two categories not included are dental and vision benefits. At the core of all Obamacare problems is more sick people signing up for insurance than healthy people signing up, specifically young millennials not signing up in sufficient numbers to make plans actuarially sound.

The main reason millennials don’t sign up is because of the obvious, they are young healthy, feel invincible and therefore don’t see the need for health insurance. But of all age groups millennials have the most diverse eating and drinking habits, making dental care a must. Many also need vision care and assistance purchasing eyeglasses.

But of all age groups millennials have the most diverse eating and drinking habits, making dental care a must. Many also need vision care and assistance purchasing eyeglasses.

Adding vision and dental benefits to the mandated categories for millennial policies only would give millennials the incentive to buy health insurance. Because millennials put more in than they take out, this is the one compromise out of all other healthcare compromises that pays for itself.

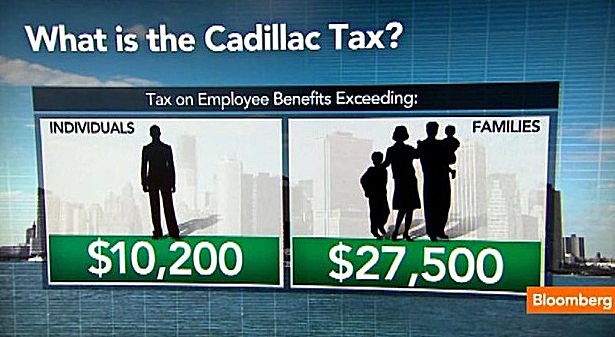

3) Repeal the tax on Cadillac health plans

A Cadillac plan is any unusually expensive health insurance plan, usually arising in discussions of medical-cost control measures in the United States. The term derives from the Cadillac automobile, which has represented American luxury goods since its introduction in 1902 and as a health care metaphor dates to the 1970’s.

The Tax Policy Center’s analysis offers the best rationale for dropping the Cadillac tax:

Under the Affordable Care Act, employer-sponsored health benefits whose value exceeds specified thresholds will be subject to an excise tax starting in 2020. This “Cadillac tax” will equal 40 percent of the value of health benefits exceeding thresholds projected to be $10,800 for single coverage and $29,050 for family coverage in 2020.

The thresholds will be indexed to growth in the consumer price index in subsequent years. Thresholds will be higher for plans with more-expensive than-average demographics, retirees ages 55 to 64, and workers in high-risk professions. The Cadillac tax will apply not only to employers’ and employees’ contributions to health insurance premiums, but also to health saving account, health reimbursement arrangement, and medical flexible spending account contributions.

The tax will be levied on insurance companies, but the burden will likely be passed on to workers in the form of lower wages. Some employers will avoid the tax by switching to less expensive health plans; this will translate into higher wages but also higher income and payroll taxes.

In fact, the Joint Committee on Taxation and the Congressional Budget Office predict that 80 percent of the revenue raised by the Cadillac tax will be through the indirect channel of higher income and payroll taxes, rather than through excise taxes collected from insurers. Simulations suggest the excise tax will have the largest relative impact on after-tax income of families in the middle income quintile.

Employer-provided health benefits are excluded from taxable income, reducing income and payroll tax revenue by an estimated $260 billion in 2017. Even if one ignores the revenue losses, there are other undesirable aspects of the exclusion.

The exclusion for employer-sponsored health insurance (ESI) is poorly targeted, as it is worth more to taxpayers in higher brackets who would be more likely to purchase insurance in the first place. Additionally, the ESI exclusions’ open-ended nature may contribute to faster health care cost growth.

Additionally, the ESI exclusions’ open-ended nature may contribute to faster health care cost growth.

For these reasons, analysts have often suggested limiting the ESI exclusion by including the value of health benefits beyond a certain threshold in taxable income (Congressional Budget Office 2013).

These are 3 healthcare compromises Democrats can make without sacrificing the core principle of providing healthcare insurance to people who can’t afford it. They are not the only ones but they are a good place to start the needed conversation with Republicans to repair Obamacare.